Warehouse Automation Market

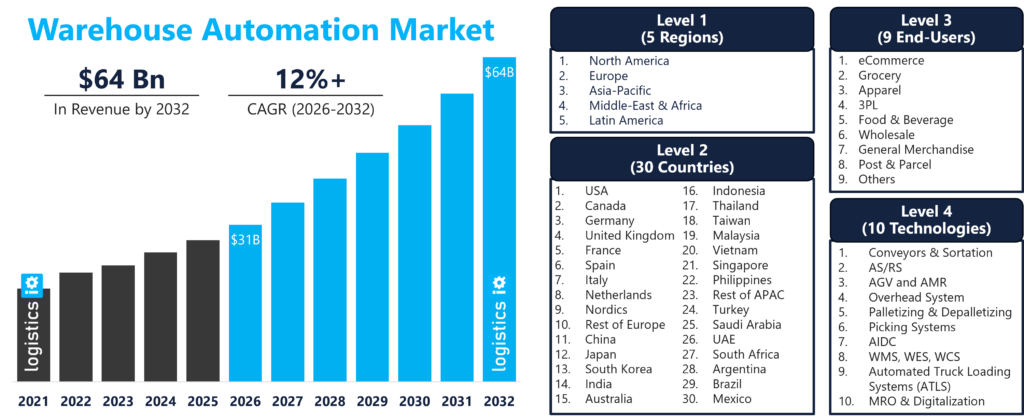

Warehouse Automation Market to reach $64B by 2032

As per LogisticsIQ latest market report, Warehouse Automation Market is expected to reach c.USD 64 billion by 2032, at a CAGR of 12.3% between 2026 and 2032.

Warehouse Automation Market – Ecosystem & Value Chain

Warehouse Automation Market Research Study : Global Forecast to 2032

The global warehouse automation market has reached a strategic inflection point. Navigating beyond a well-documented phase of macroeconomic calibration and structural realignment, the sector is entering a broad-based, high-velocity expansion phase. Direct quantitative modeling by LogisticsIQ positions the global warehouse automation market to reach $64 Billion by 2032, sustained by an accelerating CAGR of 12% from 2026 through 2032.

While market visibility often centers on high-profile installations, the underlying reality is stark: 80% of operational warehouses worldwide remain completely manual, lacking any automation support. This profound structural vacuum represents an unprecedented, multi-billion-dollar runway for enterprise commercial growth, technology replacement cycles, and private equity capital deployment.

This study serves as the definitive global reference tool across the corporate spectrum. It provides system integrators with critical competitor benchmarking, mobile robotics OEMs with clear software integration pathways, component manufacturers with exact addressable demand sizing, tier-1 management consultancies with validated modeling baselines, and investment firms with the exact data needed to evaluate enterprise multiples.

The 6th edition of our market study, synthesized from over 100 deep-dive stakeholder interviews and an exhaustive evaluation of more than 700 global players, provides a clear view to the structural shifts defining the industry today.

Warehouse Automation Drivers

The Greenfield-to-Brownfield Structural Pivot: As macroeconomic variables cause a slowdown in new global greenfield construction, the industry’s primary value pool has shifted decisively toward retrofitting existing brownfield assets. This report analyzes how layout limitations are altering the demand for traditional conveyors and driving the adoption of high-density Cube-Based AS/RS and infrastructure-free mobile fleets.

The Software-Defined Orchestration Shift: Hardware performance characteristics are standardizing, causing the industry’s competitive moat to migrate from physical machinery to software orchestration. We provide a comprehensive look at how Warehouse Execution Systems (WES) and AI machine vision platforms are converging to dictate equipment selection, completely reshaping the landscape for software developers, vision providers, and system integrators alike.

Quantifying the Automation Frontiers: Beyond established modalities, we calculate the exact financial trajectory of frontier solutions, from Autonomous Mobile Robots (AMRs) executing automated piece-picking to Automatic Truck Loading Systems (ATLS) engineered to resolve terminal dock bottlenecks. Crucially, the report tracks how MRO and Digital Services are scaling to generate high-margin, recurring revenues that protect technology vendors from cyclical project capital expenditure downturns.

KEY FINDINGS

Warehouse Automation Adoption Accelerates as Labor Shortages, eCommerce Growth, and Evolving Consumer Expectations Reshape Supply Chains

- US, Germany and China are the key market: The U.S., China, and Germany continue to lead the warehouse automation landscape, supported by their position as major global manufacturing, trade, and logistics hubs. North America remains the largest regional market, while Europe accounts for roughly one-third of global logistics activity and hosts many of the industry’s leading automation providers. Looking ahead, the fastest growth is expected in Asia-Pacific, particularly India and Southeast Asia driven by strong eCommerce growth and supply-chain modernization, while emerging markets such as the Middle East, Brazil, Mexico, Poland, and the Czech Republic are gaining prominence as companies diversify and regionalize their supply chains.

- Online Grocery becoming the top attraction for warehouse automation: Grocery remains one of the most logistics-intensive retail segments due to high order volumes, frequent replenishment cycles, and stringent freshness requirements. As online grocery sales continue to expand and retailers pursue faster fulfillment models, automation investments in micro-fulfillment centers (MFCs), robotics, and automated storage systems are accelerating. Leading retailers and solution providers—including Walmart–Symbotic, Kroger–Ocado, and Alibaba’s Freshippo, have demonstrated the strategic importance of automation, while industry estimates indicate the MFC market could exceed $10 billion by 2032, supported by growth rate of ~15%. Higher automation driven by online grocery, micro-fulfillment centers (MFC) and ultrafast deliveries is going to be biggest opportunity in next 5 years led by different type of solution providers such as AutoStore, Ocado, Exotec, Symbotic, Attabotics, OPEX, Fabric, Geek+, and Urbx Logistics.

- AGV/AMR will remain the key technology to adopt: AGV and AMR market is expected to become the fastest-growing segment of warehouse automation, driven by accelerating eCommerce fulfillment requirements, labour shortages, and the need for flexible, scalable automation. Unlike traditional fixed automation, AMRs can be deployed with minimal infrastructure changes, making them particularly attractive for small and mid-sized warehouses seeking rapid ROI and operational agility. As a result, mobile robotics is expected to account for more than 25% of the warehouse automation market by 2032, led by technology providers such as Geek+, Hai Robotics, GreyOrange, Locus Robotics, Quicktron, Hikrobot, Seegrid, MiR (Teradyne), OTTO Motors, and Omron, among others. While ASRS solutions continue to offer higher throughput, AMRs are increasingly preferred for their lower deployment costs, flexibility, and ability to support dynamic fulfillment operations. A key emerging trend is the integration of AI-enabled robotic manipulators and mobile picking robots, which combine autonomous navigation with robotic arms to automate piece-picking, sortation, depalletizing, and mixed-case order fulfillment, further expanding the scope of warehouse automation.

- Picking systems are still largely manual: Order picking remains the most labor-intensive and operationally complex activity within modern warehouses, making it a key focus area for automation investments. While manual picking continues to play an important role in high-SKU environments such as eCommerce and online grocery, warehouses are increasingly adopting goods-to-person systems, RFID-enabled identification, pick-to-light, and pick-to-voice technologies to improve productivity, accuracy, and labor efficiency in picking system market worth ~$5B by 2032. Automated storage and retrieval systems (ASRS) and robotic picking solutions are further reducing dependence on manual labor by streamlining item retrieval and order fulfillment. The latest wave of innovation is centered on AI-powered piece-picking robots and robotic manipulators capable of handling diverse products, irregular shapes, and mixed-SKU orders with greater accuracy and speed. Companies such as Dexterity, Covariant, Plus One Robotics, Berkshire Grey, RightHand Robotics, Fizyr, Osaro, and Pickr AI are advancing vision-guided robotic picking, enabling warehouses to automate increasingly complex picking tasks that were previously considered too challenging for robotics, thereby accelerating the transition toward fully autonomous fulfillment operations.

Highlights of Warehouse Automation Market Report

- Warehouse automation suppliers and industry experts expect sustained double-digit market expansion over the long term, driven by structural labor shortages, continued eCommerce growth, and accelerating digitalization of supply chains. The convergence of Physical AI, Industrial IoT, 5G connectivity, and autonomous operations is reshaping warehouse networks, making automation a strategic enabler of resilience, productivity, and customer responsiveness.

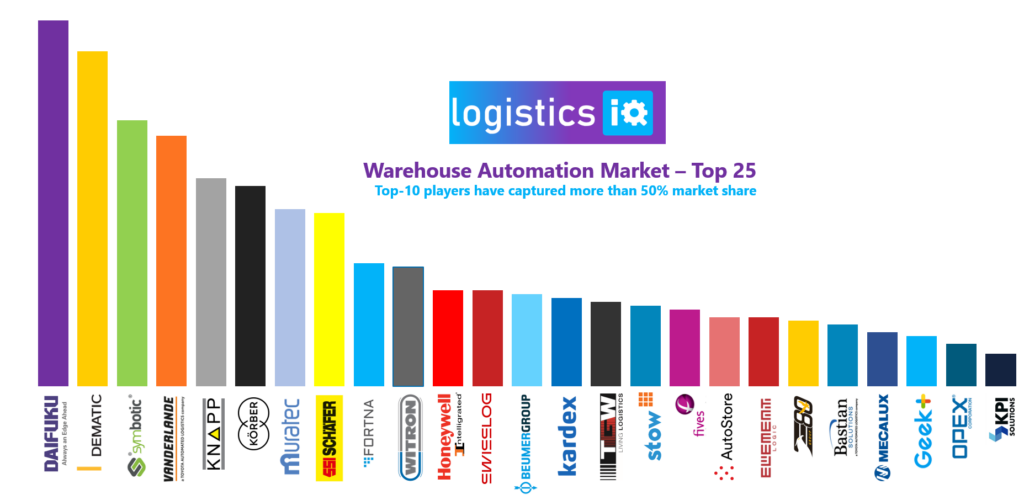

- Competitive landscape – The warehouse automation market remains moderately consolidated, with approximately 15 large players generating over US$1 billion in annual revenue and another 15–20 mid-sized providers generating US$200 million–US$1 billion. Industry leaders including Dematic, Daifuku, SSI Schaefer, Symbotic, Knapp, Vanderlande, Honeywell Intelligrated, Muratec, Beumer, Fortna, and Witron collectively command over half of the global market. At the same time, innovation is increasingly being driven by emerging specialists in AMRs, robotic picking, cube-based storage, micro-fulfillment, and AI-powered autonomy, with companies such as Symbotic rapidly establishing themselves as major competitive forces.

- Services, both MRO and Digital, importance is increasing – Over the time as the installed base of automated warehouse solutions grows, industry players expect an increase in revenues from services and maintenance, which would have a positive impact on profitability as the service business typically has 15-20% operating margins, versus 3-5% margins for new equipment. It is expected to be ~$15B opportunity by 2032 including digital services which is almost 25% of total market.

- Business models are also changing considering the real time pain points of end-users for high capex. Businesses are increasingly intrigued with RaaS (Robotics As a Service) because of its flexibility, scalability, and lower cost of entry than traditional robotics programs. The business model for pick-as-a-service is usually on a per-pick basis, ranging from 6 cents to 10 cents per pick, while AMR-as-a-service is usually leased on a monthly basis, from US$750 per robot per month to several thousands of dollars per month, depending on the commitment period.

- Industry Consolidation – The past 5 years have seen an increase in consolidation amongst material handling equipment providers as traditional players see acquisition of new technology leaders as an increasingly attractive way of positioning themselves in response to changing market trends. Acquisitions like Rockwell Automation (Clearpath Robotics, OTTO Motors), Jungheinrich (Magazino), SSI Schafer (DS Automotion), Zebra (Fetch Robotics, Matrox), ABB (ASTI), Toyota (Vanderlande, Bastian Solutions, ViaStore), Murata Machinery (Cimcorp), Locus Robotics (Waypoint), Hitachi (JR Automation), KPI Solutions (Kuecker Logistics Group, Pulse Integration, QC Software), Ocado (6 River Systems, Kindred, Haddington Dynamics), Element Logic (SDI), Honeywell (Intelligrated, Transnorm), Körber (Cohesio Group, Siemens Logistics, HighJump), Teradyne (MiR, Energid, AutoGuide Mobile Robots), Jungheinrich (Arculus), KION (Dematic), KUKA (Swisslog) are just some of the examples of this consolidation.

Top-10 players account for >50% of the market share currently, market to witness more M&As in the future

Facts to Know

- Global e-Commerce sales have grown at a CAGR of 20% over the last decade, reaching almost $5 trillion worldwide in 2021 and expected to grow to more than $10 trillion by 2030, while online shopping adoption exceeded 2.3 billion consumers globally, highlighting the continued shift toward digital retail channels. Looking ahead, eCommerce is expected to account for more than a quarter of global retail sales over the next decade, driving significant investments in automated fulfillment, robotics, last-mile logistics, and high-throughput warehouse infrastructure to support faster and more cost-efficient order fulfillment.

- Amazon Robotics has become one of the most influential forces in warehouse automation, with Amazon surpassing the milestone of 1 million deployed robots across more than 300 fulfillment and logistics facilities globally in 2025, compared to approximately 30,000 robots in 2015. The company is now integrating its new AI-powered orchestration platform, DeepFleet, which improves robotic fleet efficiency by roughly 10% through intelligent traffic management and real-time optimization. Following significant fulfillment network redesign efforts and automation investments, Amazon has materially improved operational productivity while enabling robot-assisted handling in approximately 75% of customer orders. In parallel, Amazon continues to stimulate innovation through its US$1 billion Amazon Industrial Innovation Fund (AIIF), investing in next-generation technologies spanning robotics, AI, automation, fulfillment, transportation, and supply chain solutions.

- Walmart and Symbotic have evolved one of the most significant automation partnerships in global retail logistics. After initially deploying Symbotic’s robotics platform at Walmart’s Brooksville, Florida distribution center in 2017, the collaboration expanded from a pilot deployment to a network-wide transformation initiative. Following Walmart’s decision to automate all 42 U.S. regional distribution centers, Symbotic is currently deploying its AI-enabled robotics and software platform across the entire RDC network. In 2025, the partnership deepened further when Symbotic acquired Walmart’s Advanced Systems and Robotics business and signed a strategic agreement to develop next-generation automation for Walmart’s Accelerated Pickup and Delivery (APD) facilities. Under the agreement, Walmart committed US$520 million toward the development program and plans to deploy automation systems across 400 APD centers over multiple years, potentially adding more than US$5 billion to Symbotic’s future backlog while extending automation beyond distribution centers into store-level fulfillment and last-mile operations.

- Eastern Europe is emerging as one of the most attractive warehouse automation growth regions in Europe, driven by nearshoring, eCommerce expansion, and the relocation of supply chains closer to end markets. Poland has established itself as the region’s leading logistics hub, with modern warehouse stock exceeding 36 million sq. m., ranking among the largest warehouse markets in Europe, while attracting significant investment from global retailers, 3PLs, and manufacturers. Competitive labor economics, growing labor shortages, and continued infrastructure investment are accelerating adoption of robotics, AMRs, ASRS, and warehouse software across Poland, the Czech Republic, Slovakia, and Hungary. As companies increasingly use Central and Eastern Europe as a gateway to both Western and Eastern European markets, the region is expected to deliver above-average growth in warehouse automation over the remainder of the decade.

- China has established itself as the global leader in warehouse automation, fueled by the world’s largest eCommerce ecosystem, rapid logistics modernization, and strong government support for intelligent manufacturing. A new generation of Chinese automation champions, including Geek+, Hai Robotics, Hikrobot, Quicktron, Siasun, Multiway Robotics, VisionNav Robotics, SEER Robotics, and Libiao Robotics, is driving innovation across AMRs, autonomous case-handling robots (ACRs), robotic picking, high-density storage, and AI-enabled warehouse orchestration. Geek+ has deployed solutions across more than 950 warehouses globally and processed over 10 billion orders, while Quicktron has implemented over 42,000 AMRs for more than 1,000 customers worldwide, underscoring the scale and maturity of China’s automation ecosystem. Chinese providers are increasingly expanding into Europe, North America, Southeast Asia, and the Middle East, leveraging cost-competitive, software-centric, and highly scalable automation platforms to challenge established global leaders and position China as a major exporter of warehouse automation technology.

- Warehouse automation capex remains robust despite broader economic uncertainty, as operators increasingly prioritize productivity, labour resilience, and supply-chain agility. Large-scale distribution centers are typically investing anywhere from US$10–100+ million per facility in automation, while leading retailers and logistics providers continue to commit billions of dollars toward network modernization and robotics deployment. The industry is also witnessing a shift from traditional fixed automation toward modular AMRs, AI-driven software, and goods-to-person systems that can deliver payback periods of approximately 2–5 years. Combined with the rapid adoption of Robotics-as-a-Service (RaaS) and subscription-based models, which can lower upfront investments by up to 60–80%, these financing and technology trends are expected to significantly expand automation penetration and sustain double-digit market growth over the next five years.

What will you get in this report?

- LogisticsIQ™ Exclusive Market Map (700+ Players across 15+ categories)

- 500+ Pages and 290+ Exhibits Market Report for 8 major Industry Verticals and 10 Technologies

- A bottom-up analysis of Warehouse Automation market for 30 countries and regions

- In-depth analysis of 700 companies in the ecosystem with more than 140 company profiles

- Focus Group Discussion with 100+ key industry stakeholders across the value chain to collect the first-hand information to validate our analysis

- Excel file with a pivot modelling and 350+ market tables including forecast till 2032

- 2 Analyst Sessions

- Investment details with 150+ M&A and 750+ funding deals

- Executive Summary

- 1.1 Market Dynamics

- 1.1.1 Change in Market Dynamics

- 1.1.2 Geopolitical Pressures, Tariffs, and Pricing Impacts

- 1.1.3 Forecast Revisions and Lowered Adoption Curves

- 1.2 A Market at a Strategic Inflection Point

- 1.3 Three Key Forces Driving Unprecedented Demand

- 1.4 The Technology Paradigm Shift

- 1.5 The Future is Intelligent and Autonomous

- 1.1 Market Dynamics

- Warehouse Automation Overview

- 2.1 Anatomy of warehouse operations

- 2.1.1 Types of Warehouses

- 2.1.2 Key Areas in a Warehouse or Distribution Center

- 2.1.3 Picking Systems – Still Largely Manual

- 2.1.4 Automated Sorting – Widely Adopted

- 2.1.5 Palletizing Systems – Smarter and More Integrated

- 2.1.6 Automated Storage and Retrieval Systems (AS/RS) – Critical for Fulfillment

- 2.1.7 Warehouse Management Systems (WMS) – The Digital Backbone

- 2.1.8 Key Benefits of Warehouse Automation

- 2.2 Warehouse Management System (WMS) , Warehouse Execution Systems (WES) and Warehouse control systems (WCS)

- 2.3 Automatic Identification and Data Capture (AIDC)

- 2.4 Conveyors, Sorting and Overhead Systems

- 2.5 Mobile Robots – Autonomous Guided Vehicles (AGVs) and Autonomous Mobile Robots (AMRs)

- 2.5.1 Goods-to-Person (G2P) Robots

- 2.5.2 Person-to-Goods (P2G) / Collaborative Picking Robots

- 2.5.3 Sortation Robots

- 2.5.4 Autonomous Case-handling Robots (ACRs)

- 2.5.5 Autonomous Forklifts & Pallet Movers

- 2.5.6 Tugger AGVs/AMRs

- 2.6 Automated Storage and Retrieval System (AS/RS)

- 2.6.1 Unit-Load ASRS

- 2.6.2 Mini-Load Cranes

- 2.6.3 Shuttle-Based Systems

- 2.6.4 Cube-Based ASRS

- 2.6.5 Robotic Mobile Rack ASRS

- 2.6.6 Vertical Storage Systems

- 2.7 Palletizing/Depalletizing Systems

- 2.8 Order Picking

- 2.8.1 Picker-to-Parts Methodologies (Human-Centric Augmentation)

- 2.8.2 Robotic Picking Methodologies

- 2.8.3 Currently available technologies are capable of delivering fully automated picking solutions

- 2.9 Automatic Truck Loading System (ATLS)

- 2.10 MRO, Digital Services, and Lifecycle Management

- 2.11 Emerging Technologies & The Future of Automation

- 2.11.1 Humanoid Robots

- 2.11.2 Other Key Emerging Technologies

- 2.1 Anatomy of warehouse operations

- Warehouse Automation Business Model

- 3.1 The Traditional Model: Project-Based System Integration

- 3.1.1 Operating Model & Value Proposition

- 3.1.2 Economic Model & Strategic Insights

- 3.2 The Disruptive Model: Flexible Automation “As-a-Service”

- 3.2.1 Robotics-as-a-Service (RaaS)

- 3.2.2 Performance-Based & Outcome-Based Models

- 3.3 The Hybrid Model: Software-as-a-Service (SaaS) for Automation

- 3.3.1 Operating Model & Value Proposition

- 3.4 The OEM Model: Powering the Ecosystem

- 3.4.1 Operating Model & Value Proposition

- 3.5 The Brownfield Model: Modular Deployment & Phased Modernization

- 3.5.1 Operating Model & Value Proposition

- 3.5.2 Economic Model & Strategic Insights

- 3.1 The Traditional Model: Project-Based System Integration

- Warehouse Automation Market – Drivers and Challenges

- 4.1 Key Drivers – The Unstoppable Forces Propelling the Automation Imperative

- 4.1.1 Labor Crisis

- 4.1.2 The eCommerce & Omnichannel Revolution

- 4.1.3 Faster adoption of online grocery worldwide

- 4.1.4 The Strategic Imperative of Supply Chain Resilience

- 4.1.5 The Decarbonization Mandate: Automation as an ESG Enabler

- 4.2 Key Market Challenges – Navigating the Hurdles to Widespread Adoption

- 4.2.1 High Upfront Capital Investment & Economic Headwinds

- 4.2.2 Operational Flexibility & The Pace of Innovation

- 4.2.3 Integration Complexity

- 4.2.4 Cybersecurity Risks

- 4.1 Key Drivers – The Unstoppable Forces Propelling the Automation Imperative

- Major End-Customers in Warehouse Automation Market

- 5.1 Amazon

- 5.1.1 The Expanding (Accelerating) Role of Robot-Enabled Fulfilment

- 5.1.2 The Benefits of Automation/Robotics

- 5.1.3 Amazon Industrial Innovation Fund

- 5.1.4 There Is Still Room for Improvement

- 5.1.5 Fleet Scaling and Generative AI Infrastructure

- 5.1.6 Amazon – New Technology Deployment and Humanoid Pilots

- 5.1.7 Future Outlook: Next Generation AMRs and Prime Air Expansion

- 5.2 JD.com

- 5.2.1 Automated Warehouse development

- 5.2.2 Deployment of Delivery Drones

- 5.2.3 Autonomous Delivery Robots in Changsha and Hohhot

- 5.3 Walmart

- 5.3.1 Next Gen Fulfillment Centers and partnership with Symbotic

- 5.3.2 Future Outlook & Announced Projects

- 5.3.3 Alphabot Micro-Fulfilment Centre – Transition from Alert Innovation to Symbotic

- 5.4 Tesco

- 5.5 Kroger

- 5.5.1 Kroger-Ocado Partnership

- 5.5.2 Delivery Logistics: Expanded Third-Party Partnerships

- 5.5.3 Autonomous Last Mile Delivery

- 5.5.4 Optimization and In-Store AI Adaptations

- 5.6 Ocado

- 5.6.1 Ocado Smart Platform (OSP)

- 5.6.2 Ocado is distributing and licensing its technology to other retailers

- 5.7 ASOS

- 5.8 Zalando

- 5.8.1 Zalando and Magazino Partnership

- 5.9 DHL Supply Chain

- 5.9.1 DHL and Locus Robotics Partnership

- 5.1 Amazon

- Warehouse Automation Market, by Technology

- 6.1 Conveyors and Sortation Systems

- 6.2 Overhead Systems

- 6.2.1 Gantry Robots

- 6.3 Automated Storage and Retrieval System (AS/RS)

- 6.4 Palletizing/De-palletizing Systems

- 6.5 Automatic Identification and Data Capture

- 6.6 Autonomous Guided Vehicles (AGV) & Autonomous Mobile Robots (AMR)

- 6.7 Order Picking

- 6.8 WMS, WES, WCS

- 6.9 Automated Truck Loading Systems

- 6.10 MRO services

- Warehouse Automation Market, by End-user Industry

- 7.1 E-Commerce

- 7.1.1 Amazon

- 7.1.2 Alibaba (Cainiao Network)

- 7.1.3 JD.com

- 7.2 Grocery

- 7.2.1 Walmart

- 7.2.2 Kroger

- 7.2.3 Ocado Group

- 7.3 Food and Beverage

- 7.3.1 PepsiCo

- 7.3.2 Nestlé

- 7.3.3 Anheuser-Busch InBev

- 7.4 Fashion & Apparel

- 7.4.1 Inditex (Zara)

- 7.4.2 Nike

- 7.4.3 Zalando

- 7.5 3PL

- 7.5.1 DHL Supply Chain

- 7.5.2 GXO Logistics

- 7.5.3 Kuehne+Nagel

- 7.6 General Merchandise

- 7.6.1 Target

- 7.6.2 The Home Depot

- 7.7 Post & Parcel

- 7.7.1 UPS

- 7.7.2 FedEx

- 7.7.3 DHL Express

- 7.8 Wholesale

- 7.8.1 W.W. Grainger:

- 7.9 Others (incl. Pharma & Lifesciences, Metals & Mining, Chemicals)

- 7.9.1 McKesson (Pharmaceuticals)

- 7.9.2 BASF (Chemicals)

- 7.1 E-Commerce

- Warehouse Automation Market Size, by country

- 8.1 North America

- 8.1.1 USA

- 8.1.2 Canada

- 8.2 Europe

- 8.2.1 Western Europe: Maximizing Tight Urban Footprints

- 8.2.2 Central & Eastern Europe: The Rapidly Expanding Regional Hub

- 8.2.3 UK

- 8.2.4 Germany

- 8.2.5 France

- 8.2.6 Italy

- 8.2.7 Spain

- 8.2.8 Netherlands

- 8.2.9 Nordic

- 8.2.10 Rest of Europe

- 8.3 Asia-Pacific

- 8.3.1 China

- 8.3.2 Japan

- 8.3.3 South Korea

- 8.3.4 India

- 8.3.5 Australia

- 8.3.6 South East Asia

- Vietnam

- Indonesia

- Thailand

- Taiwan

- Singapore

- Malaysia

- 8.4 Middle East & Africa

- 8.4.1 The Middle East Is Building Regional Logistics Hubs to Diversify Beyond Oil

- 8.4.2 Economic Diversification, E-commerce and Localization Are Reshaping Warehouse Investments

- 8.4.3 Automation Demand Is Led by 3PL, Retail, E-commerce and Food Logistics

- 8.4.4 Country-Level Differences

- 8.4.5 Saudi Arabia

- 8.4.6 UAE

- 8.4.7 Turkey

- 8.4.8 South Africa

- 8.5 Latin America

- 8.5.1 Latin America Is Modernizing Historically Fragmented Logistics Networks

- 8.5.2 E-commerce, Nearshoring and Retail Modernization Are Reshaping Warehouse Investments

- 8.5.3 Automation Demand Is Led by E-commerce, Retail, 3PL and Manufacturing Logistics

- 8.5.4 Country-Level Differences

- 8.5.5 Mexico

- 8.5.6 Brazil

- 8.5.7 Argentina

- 8.1 North America

- Competitive Landscape

- 9.1 Automation Solutions Matrix by key players

- 9.1.1 System Integrators

- 9.1.2 Warehouse Management Software Solutions

- 9.1.3 Automatic Identification and Data Capture (AIDC)

- 9.2 Market Share Analysis

- 9.3 Regional Landscape

- 9.3.1 North America

- 9.3.2 Western Europe

- 9.3.3 United Kingdom

- 9.3.4 China

- 9.3.5 Regional Players

- 9.4 System Integrators – Top Players

- 9.4.1 Daifuku

- 9.4.2 Dematic (KION Group)

- 9.4.3 SSI Schaefer

- 9.4.4 Vanderlande (Toyota Industries)

- 9.4.5 Symbotic

- 9.4.6 Fortna

- 9.4.7 Murata Machinery (Muratec)

- 9.4.8 Knapp

- 9.4.9 TGW Logistics Group

- 9.4.10 Honeywell Intelligrated (American Industrial Partners)

- 9.5 AGV & AMR – Top Players

- 9.5.1 Geek+ (China)

- 9.5.2 Locus Robotics (USA)

- 9.5.3 Hai Robotics (China)

- 9.5.4 Hikrobot (China)

- 9.5.5 GreyOrange (US/India)

- 9.5.6 Tier 2: Specialized & High-Growth Innovators

- 9.6 AIDC & Vision System – Top Players

- 9.6.1 Zebra Technologies (USA)

- 9.6.2 Datalogic S.p.A. (Italy)

- 9.6.3 SICK (Germany)

- 9.6.4 Honeywell SPS (USA)

- 9.6.5 SATO (Japan)

- 9.6.6 Cognex (USA)

- 9.6.7 Keyence Corporation (Japan)

- 9.6.8 Basler AG (Germany)

- 9.7 Software (WMS/WES/WCS) – Top Players

- 9.7.1 Blue Yonder (USA)

- 9.7.2 Manhattan Associates (USA)

- 9.7.3 Oracle (USA)

- 9.7.4 SAP (Germany)

- 9.7.5 Körber Supply Chain – HighJump (Germany)

- 9.7.6 Infor (USA)

- 9.8 Industrial Robots (Articulated Arms) – Top Players

- 9.8.1 Fanuc (Japan)

- 9.8.2 ABB (Sweden/Switzerland)

- 9.8.3 Kuka (Germany)

- 9.8.4 Yaskawa (Japan)

- 9.8.5 Epson Robots (Japan)

- 9.8.6 Universal Robots (Denmark)

- 9.9 Automated Loading & Unloading (ATLS) – Top Players

- 9.9.1 Ancra Systems B.V. (Netherlands)

- 9.9.2 Joloda Hydraroll (UK) and Actiw Oy (Finland)

- 9.9.3 Boston Dynamics (USA)

- 9.9.4 Dexterity (USA)

- 9.9.5 Pickle Robot (USA)

- 9.9.6 Slip Robotics (USA)

- 9.9.7 Fox Robotics (USA)

- 9.1 Automation Solutions Matrix by key players

- Scope & Definition

- Research Methodology

- Company Profiles – System Integrators

- 12.1 Daifuku

- 12.1.1 Introduction

- 12.1.2 General Information

- 12.1.3 Financial Results by reportable segments

- 12.1.4 Daifuku Sales and Orders by Industry (In Billion Yen)

- 12.1.5 Business Plan – Value Transformation

- 12.1.6 The Innovation Center

- 12.1.7 Geographical Presence

- 12.1.8 Key Development in 2025

- 12.1.9 Major Development & News in the past

- 12.1.10 Product Portfolio By Industry

- 12.1.11 Product Portfolio By Function

- 12.1.12 Industries & Solutions Offered

- 12.1.13 Successful Case Studies (Customer List)

- 12.2 Dematic (KION Group)

- 12.3 SSI-Schaefer

- 12.4 Vanderlande (Toyota Advanced Logistics)

- 12.5 Swisslog (KUKA)

- 12.6 Knapp AG

- 12.7 Murata Machinery Ltd.

- 12.8 Elettric 80

- 12.9 Beumer Group

- 12.10 Witron Logistik + Informatik

- 12.11 TGW Logistics

- 12.12 Grenzebach GmbH

- 12.13 FIVES Group

- 12.14 Honeywell Intelligrated

- 12.15 Bastian Solutions (Toyota Advanced Logistics)

- 12.16 Wayzim Technology

- 12.17 FORTNA (Material Handling System – MHS)

- 12.18 Jungheinrich AG

- 12.19 LODIGE Industries

- 12.20 Viastore Systems (Toyota Advanced Logistics)

- 12.21 Körber AG

- 12.22 Symbotic

- 12.23 Interlake Macalux

- 12.24 Kardex

- 12.25 AutoStore

- 12.26 DMW&H

- 12.27 Westfalia

- 12.28 Dambach AG

- 12.29 PSB intralogistics GmbH

- 12.30 SIASUN Robot Automation Co., Ltd.

- 12.31 KPI Integrated Solutions

- 12.32 SAVOYE

- 12.33 OPEX Corporation

- 12.34 System Logistics (Krones Group)

- 12.35 Addverb Technologies

- 12.36 Lodamaster Group

- 12.37 GÜDEL

- 12.1 Daifuku

- Company Profiles – AGV & AMR

- Geek+

- Quicktron (Flashhold)

- ForwardX Robotics

- Huaxiao Precision (Suzhou) Co., Ltd. – (CSG Huaxiao)

- GreyOrange

- HIKROBOT (HIKVISION)

- Mobile Industrial Robots – MiR (Teradyne)

- inVia Robotics

- 6 River Systems (OMRS – Ocado Mobile Robot System)

- Fetch Robotics (Zebra Technologies)

- JBT Marel (John Bean Technologies & Marel)

- JATEN

- Onward Robotics (IAM Robotics)

- Locus Robotics

- Vecna Robotics

- BALYO (SoftBank Group)

- SEEGRID

- Waypoint Robotics (Locus Robotics)

- Tompkins Robotics

- Scallog

- OTTO Motors (Clearpath Robotics) – Rockwell Automation

- GIDEON Brothers

- Magazino – A Jungheinrich Company

- JASCI Robotics (NextShift Robotics)

- AutoGuide Mobile Robots (MiR, Teradyne)

- EiraTech Robotics

- Aethon (ST Engineering)

- Prime Robotics (BLEUM)

- HAI Robotics

- Bionic HIVE

- Oppent

- PAL Robotics

- Matthews Automation Solutions (Duravant)

- GUOZI Robotics (Hangcha)

- CAJA Robotics (Fives Intralogistics)

- Omron Robotics (Adept Technology)

- Guidance Automation (Matthews International)

- Syrius Technology

- MALU Innovation (JD Logistics)

- Eurotec (Lowpad)

- DS Automotion GmbH (SSI Schaefer)

- Rocla (Mitsubishi Logisnext Europe Oy)

- Neobotix

- SCOTT Group (Transbotics)

- ek-robotics (NEURA)

- OCEANEERING MOBILE ROBOTICS

- Wellwit Robotics

- Logistic-Jet

- Mushiny

- TÜNKERS Maschinenbau GmbH

- CPM – Dürr Group

- Shanghai Seer Intelligent Technology Corporation (SEER)

- FlexQube

- AUMOVIO Robotic Solutions (Formerly Continental Mobile Robots)

- IDEALworks GmbH (Agile Robots)

- Company Profiles – Autonomy Service Providers (ASP)

- Brain Corporation

- Bluebotics – a ZAPI Group Company

- Kollmorgen – A Regal Rexnord Brand

- Autonomous Solutions, Inc. (ASI)

- MOVEL AI

- MOV AI

- FREEDOM ROBOTICS

- ROBOMINDS

- PERCEPTIN

- Hangzhou Coevolution Technology Co., Ltd.

- FORT Robotics

- Romb Technologies

- Company Profiles – Machine Vision & Imaging

- Basler AG

- Keyence

- Omron Automation (Microscan Systems)

- Cognex

- Company Profiles – Disinfection Robots

- UVD Robotics (Blue Ocean Robotics)

- Palladyne AI (Sarcos Robotics)

- Techmetics Robotics

- Wellwit Disinfection Robotics

- Company Profiles – Retail Robots

- Bossa Nova Robotics

- Simbe Robotics

- Badger Technologies (Jabil)

- Lowe’s – LoweBot (Powered by Fellow AI)

- Company Profiles – Indoor Delivery Robots

- Bear Robotics

- Keenon Robotics

- Relay Robotics (Savioke Inc.)

- Rice Robotics

- Company Profiles – Security and Inspection Robots

- Cobalt AI (Dean Drako)

- Knightscope Robotics

- OTSAW Digital

- SMP Robotics

- Company Profiles – Tele-operated / Telepresence Robots

- Diligent Robotics

- Ohmni Labs

- AVA Robotics

- GoBe Robotics (Blue Ocean Robotics)

- Company Profiles – Cleaning Robots

- Softbank Robotics

- Avidbots

- Gaussian Robotics

- LionsBot

- Company Profiles – Hospital Support Robots

- Revotonix L.L.C

- Solaris Robots (Jetbrain Robotics)

- Company Profiles – Agriculture Robots

- Bogaerts

- Harvest Automation

- Company Profiles – Battery & Chargers

- LG Chem (LG Energy Solutions)

- Crown Equipment Corporation

- East Penn Manufacturing

- EnerSys

- Conductix-Wampfler

- Company Profiles – Key Components

- Advance Motion Control

- Kollmorgen (Regal Rexnord Motion Segment)

- Energid (Teradyne)

- Harmonic Drive System

- Murrelektronik

- Company Profiles – Piece Picking Robots

- Berkshire Grey (SoftBank)

- Righthand Robotics

- KINDRED (Ocado Group)

- OSARO

- Plus One Robotics

- Company Profiles – Warehouse Management System Providers

- Blue Yonder (JDA)

- Intelligent Fulfillment™ WMS

- Infor (Koch Industries)

- CloudSuite™ WMS

- Oracle

- Oracle Warehouse Management Cloud (WMS)

- SAP

- SAP Extended Warehouse Management (SAP EWM)

- Manhattan Associates

- Manhattan SCALE™ WMS

- Körber Supply Chain (HighJump)

- Körber Logistics System

- HighJump WMS

- Blue Yonder (JDA)

- Company Profiles – Automatic Identification and Data Capture (AIDC)

- Zebra Technologies

- Honeywell AIDC

- Data Logic

- SATO

- SICK AG

- Company Profiles – Warehouse Drones

- Eyesee (HARDIS Group)

- UVL ROBOTICS

- AirMap (DroneUp)

- Company Profiles – Delivery Robots

- Starship Technologies

- NURO AI

- Tele Retail

- Kiwibot

- Robby Technologies

- List of Exhibits

- EXHIBIT 1: Warehouse Automation Market to grow >2x at ~12% CAGR

- EXHIBIT 2:AGV/AMR and MRO services making up for the biggest share of the market

- EXHIBIT 3:eCommerce and Grocery are accounting for the highest demand

- EXHIBIT 4: APAC will account for the largest demand, while Latin America will be fastest growing region

- EXHIBIT 5:Systems and technologies making up Warehouse automation

- EXHIBIT 6:Process steps inside a warehouse

- EXHIBIT 7:Warehouse automation – Digitalization and Automation

- EXHIBIT 8:Warehouse automation Software Stack is converging

- EXHIBIT 9: Barcodes optimize the identification of pallets

- EXHIBIT 10: Wearable Devices in Warehouses

- EXHIBIT 11: Main causes of error in behind order fulfillment

- EXHIBIT 12: Conveyor and Sortation

- EXHIBIT 13: Advanced Conveyor Systems

- EXHIBIT 14: Mixed Case Palletizing Robot with Conveyor

- EXHIBIT 15: AGV vs AMR

- Exhibit 16: Fetch Robotics’ Fetch and Freight

- Exhibit 17: Adept’s Lynx

- EXHIBIT 18: Geekplus’s Mobile Robot

- EXHIBIT 19: Mobile Industrial Robots (MIR)’S MIR200

- EXHIBIT 20: Illustration of AS/RS for Pallets with Loading Docks and Conveyor System

- EXHIBIT 21: Swisslog Shuttle AS/RS for Order Picking

- EXHIBIT 22: A Glimpse of Körber’s stacker crane

- EXHIBIT 23: Liberty Research Mixed Case Palletising with Picking Robot

- EXHIBIT 24: Warehouse split case labour hours, by function

- EXHIBIT 25: Pick-to-light solutions are very useful for pharmaceutical companies

- EXHIBIT 26: Autonomous Picking Robots from Fetch

- EXHIBIT 27: AGVs from Amazon Robotics (formerly KIVA)

- EXHIBIT 28: Overview of Order Picking Systems by Category

- EXHIBIT 29: Classification of Automated Order Picking Systems by Number of SKUs and Throughput

- EXHIBIT 30: Overview of ATLS Technology

- EXHIBIT 31: Overview of MRO Services

- EXHIBIT 32: Introduction to Humanoid Robots

- EXHIBIT 33: Mobile Manipulators in Warehouses

- EXHIBIT 34: Drones for Warehouse Operations

- EXHIBIT 35: System Integrator Business Model

- EXHIBIT 36: Number of RaaS companies by market segment

- EXHIBIT 37: RaaS for warehouse automation

- EXHIBIT 38: Hybrid Business Model

- EXHIBIT 39: System OEM Business Model

- EXHIBIT 40: Component OEMs Business Model

- EXHIBIT 41: Four levels of Warehouse Automation defined

- EXHIBIT 42: Warehouse automation market will grow to ~$64 billion by 2032

- EXHIBIT 43: 10-Year U.S. Warehousing Sector Labor & Shortage Trends (2016–2026)

- EXHIBIT 44: eCommerce adoption continues unabated; however, growth is stagnating

- EXHIBIT 45: eGrocery adoption driving the warehouse automation market

- EXHIBIT 46: USA and East Asia will continue to drive the online grocery adoption

- EXHIBIT 47: Modern Supply Chain

- EXHIBIT 48: Cost Breakdown of 10,000 Pallet AS/RS (Million Euros)

- EXHIBIT 49: Hikrobotics’ Qianmo Smart Warehouse Robot

- EXHIBIT 50: Quicktron Robot

- EXHIBIT 51: Warehouse Integration Complexity

- EXHIBIT 52: Inventory Carrying Costs

- EXHIBIT 53: CBRE – Logistics Property Sector Performance Drivers

- EXHIBIT 54: Online Aggregation Model

- EXHIBIT 55: Product Range by Retailer: U.K. Clothing

- EXHIBIT 56: Total Global Logistics Footprint of leading retailers (Million Sq. Feet)

- EXHIBIT 57: Amazon Robotics Solutions – Digit and Sequoia

- EXHIBIT 58: Number of Robots in Amazon’s FCs

- EXHIBIT 59: Amazon Robotics – Manufacturing Plant

- EXHIBIT 60: The Amazon Fulfillment Process

- EXHIBIT 61: Amazon – Last Mile Delivery

- EXHIBIT 62: JD.com Asia No.1 Warehouse in Shanghai

- EXHIBIT 63: JD.com Automated Logistics and Warehouse

- EXHIBIT 64: JD.com Mobile Robots

- EXHIBIT 65: JD.com Six axis robot

- EXHIBIT 66: JD.com Delivery Robot

- EXHIBIT 67: JD.com Delivery Drone

- EXHIBIT 68: Symbotic – Autonomous Robotic Warehouse Automation System

- EXHIBIT 69: Walmart Automated Fulfillment Center with Alphabot (Alert Innovation)

- EXHIBIT 70: How Consolidation Centers Fit into Walmart’s Supply Chain

- EXHIBIT 71: Tesco – Further enhancing the business with technology and AI

- EXHIBIT 72: Tesco – Testing and Learning multiple on-demand delivery platforms

- EXHIBIT 73: Tesco – Business models and delivery platform offerings

- EXHIBIT 74:Ocado Fulfillment Center for Kroger

- EXHIBIT 75:Kroger – Last Mile Delivery with Nuro AI

- EXHIBIT 76:Last Mile Delivery with Drones

- EXHIBIT 77: Andover’s CFC3 operates with1,000 Robots (bots) to Deliver 65,000 Orders per Week

- EXHIBIT 78: Each Bot has the Ability to Carry and to Lower or Lift Totes to or from Locations in the 3D Storage Grid

- EXHIBIT 79:Ocado – Right fulfilment for the right market

- EXHIBIT 80: Andover was Operating with 300 Bots on a single picking shift

- EXHIBIT 81: Suggesting a Capacity Utilization Approaching 15% as the facility ramps up

- EXHIBIT 82: Ocado’s platform (OSP) Evolution from 2018 to 2026

- EXHIBIT 83: Change in shopper lead time from 2018 to 2026 due to OSP integration

- EXHIBIT 84: Ocado: Announced roll out plans equivalent to 57 CFCs so far

- EXHIBIT 85: ASOS expansion is being fuelled by investment in distribution centers

- EXHIBIT 86: Latest Technologies with AI Studio – Enabling Shopping Experience and Leading Delivery Propositions

- EXHIBIT 87: Building a new commercial model: More efficient operations

- EXHIBIT 88: ASOS – Transformation of Investment into Efficiency

- EXHIBIT 89: Zalando’s Warehouse Automation – Inside Look

- EXHIBIT 90: Zalando – Warehouse Automation with Magazino Mobile Robot

- EXHIBIT 91: Zalando – E-commerce Logistics Infrastructure; Plan for new fulfillment centers

- EXHIBIT 92: DHL – Digitalization & Robotics Strategy

- EXHIBIT 93: DHL – Scalability and Integration are the focus areas

- EXHIBIT 94: Warehouse Automation Market to grow >2x at ~12%+ CAGR…

- EXHIBIT 95: …with AGV/AMR and MRO services making up for the biggest share of the market…

- EXHIBIT 96: …and eCommerce accounting for the highest demand

- EXHIBIT 97: Trends driving adoption of Conveyor/Sortation systems in Warehouse Automation

- EXHIBIT 98: Technology implications for conveyors and sortation systems

- EXHIBIT 99: Conveyors and sortation equipment is the basic building block of automated warehouse, to remain a large opportunity, albeit a moderate growth rate

- EXHIBIT 100: Robotic solutions are disrupting the market for Conveyor/Sortation systems

- EXHIBIT 101: Vendor Landscape for Conveyor/Sortation systems

- EXHIBIT 102: Demand drivers for Overhead system adoption

- EXHIBIT 103: Online fast fashion is driving the adoption of Overhead conveyor systems

- EXHIBIT 104: From overhead conveyance to overhead-based fulfillment orchestration

- EXHIBIT 105: Vendor landscape for Overhead solutions

- EXHIBIT 106: Gantry Robots – Best combination of payload, flexibility and stroke

- EXHIBIT 107: AS/RS solutions are being preferred for higher accuracy and faster fulfilment of orders

- EXHIBIT 108: AS/RS Technology Taxonomy

- EXHIBIT 109: AS/RS adoption is driven by throughput and ROI

- EXHIBIT 110: AS/RS Vendor Landscape

- EXHIBIT 111: Labor scarcity, case-level complexity, and mixed-SKU pallet flows driving automation adoption

- EXHIBIT 112: Palletising and De-palletising systems are needed for large warehouses

- EXHIBIT 113: Simple palletizing standardizes; mixed-case and depalletizing remain high-value frontier

- EXHIBIT 114: Differentiation moving from robot arm performance to integrated perception and orchestration

- EXHIBIT 115: Palletizing/De-palletizing Vendor landscape

- EXHIBIT 116: Real-time inventory accuracy, traceability, and automation-grade data requirements

- EXHIBIT 117: AIDC solutions to grow as well, driven in large by higher penetration in warehouse workers

- EXHIBIT 118: From manual scan-and-record to identify, validate, contextualize, and trigger action

- EXHIBIT 119: From hardware durability to integrated data platforms and automation interoperability

- EXHIBIT 120: Strategic influence concentrated among vendors with integrated identification capabilities

- EXHIBIT 121: AGV and AMR is the fastest growing segment, and is necessary for fully automated warehouses

- EXHIBIT 122: Automating movement without committing every warehouse to fixed conveyor-heavy infrastructure

- EXHIBIT 123: The value pool is migrating from mobile robot hardware to fleet-level execution intelligence

- EXHIBIT 124: Fragmented market with consolidation pressure as buyers demand scalable, integrated fleets

- EXHIBIT 125: Order picking demand driven by gap between customer expectations and manual delivery limitations

- EXHIBIT 126: Order picking technologies are seeing higher adoption as picking accuracy becomes critical

- EXHIBIT 127: Market shifting from manual picking to goods-to-person (G2P) and robotic piece picking

- EXHIBIT 128: No single architecture dominates all warehouse profiles—vendor selection is use-case specific.

- EXHIBIT 129: Warehouse Automation Software to be a ~$4b opportunity

- EXHIBIT 130: Warehouse complexity outpacing legacy system capabilities, demand for real-time orchestration software

- EXHIBIT 131: Buyers want modular capabilities that can be upgraded without destabilizing the entire stack

- EXHIBIT 132: Software shift towards adaptability and orchestration capabilities

- EXHIBIT 133: Warehouse Software Vendor landscape consolidating around enterprise suites

- EXHIBIT 134: Growth is being driven by dock labor scarcity, faster dispatch requirements

- EXHIBIT 135: Dock congestion, labor scarcity, and repeatable outbound flows drive up demand for ATLS

- EXHIBIT 136: Trend towards dock flow automation and robotic solutions is driving innovation

- EXHIBIT 137: Value shift towards software driven solutions rather than pure hardware

- EXHIBIT 138: ATLS specialists have depth in loading mechanics, integrators and robotics vendors also entering

- EXHIBIT 139: MRO services provide recurring revenue streams, and essential to business model and sustainable margins

- EXHIBIT 140:Warehouse Automation Market by End-User Industry ($Million)

- EXHIBIT 141:Each industry has different pain points and different automation needs

- EXHIBIT 142: eCommerce is the largest segment in Warehouse Automation, growing at mid double digits YoY

- EXHIBIT 143: eCommerce automation makes fragmented, high-speed fulfillment operationally viable

- EXHIBIT 144 : eCommerce Pain points and Warehouse Automation solutions

- EXHIBIT 145:Value pool is shifting from single automation assets to integrated fulfillment

- EXHIBIT 146: Grocery is the highest growth segment; higher automation is necessary for faster fulfilment

- EXHIBIT 147: Grocery automation growth driven by E-grocery, freshness risk, and local delivery economics

- EXHIBIT 148 : Grocery Pain points and Warehouse Automation solutions

- EXHIBIT 149: Grocery automation demand is highest for scalable solutions

- EXHIBIT 150 : F&B Characteristics and Warehouse Automation solutions

- EXHIBIT 151: F&B Core Demand Drivers for Automation

- EXHIBIT 152: Automation in F&B is driven by throughput and labor economics rather than pure storage expansion

- EXHIBIT 153: F&B creates strong demand for pallet automation, AS/RS, AGVs, and mixed-case palletizing

- EXHIBIT 154 : Apparel Pain points and Warehouse Automation solutions

- EXHIBIT 155: Forecasting and SKU complexity remains critical demand driver for automation solutions

- EXHIBIT 156: High volume, high SKUs and high cost of returns pushing apparel players to automate operations

- EXHIBIT 157: Apparel creates some of the strongest demand for RFID, pocket sorters, overhead systems, and returns automation

- EXHIBIT 158 : 3PL Pain points and Warehouse Automation solutions

- EXHIBIT 159: 3PL automation needs scalable solutions that reduce dependence on labor availability

- EXHIBIT 160: Automation in 3PL is driven by higher focus on operational efficiencies and faster delivery times

- EXHIBIT 161: 3PL automation needs scalable solutions that reduce dependence on labor availability

- EXHIBIT 162 : General Merchandise Characteristics and Warehouse Automation solutions

- EXHIBIT 163: Automation demand spans every process due to product diversity and fulfillment complexity

- EXHIBIT 164: General Merchandise presents a significant opportunity however, adoption is slow

- EXHIBIT 165: General merchandise is the broadest automation opportunity as every technology category has a role

- EXHIBIT 166 : F&B Characteristics and Warehouse Automation solutions

- EXHIBIT 167: Demand arises from mail sorting, address recognition, sequencing

- EXHIBIT 168: Post and Parcel is slow to adopt automation in sorting centers, limited by the ROI benefits

- EXHIBIT 169: Automation is dominated by OCR, mail sortation, sequencing, and address intelligence technologies.

- EXHIBIT 170: Demand is concentrated in storage, case picking, and pallet formation

- EXHIBIT 171: Wholesale distribution of goods is a slow growth segment as demand for faster delivery is limited

- EXHIBIT 172: Others segment has niche end-markets and growth is expected to remain stagnant

- EXHIBIT 173: APAC will account for the largest demand for warehouse automation equipment, while US will be the single largest country

- EXHIBIT 174: North America Warehouse Automation Market Size in US$ Million

- EXHIBIT 175: US Warehouse Automation Market Size in US$ Million

- EXHIBIT 176:Warehouse Automation Market in United States by End-Use Industry ($Million)

- EXHIBIT 177:Warehouse Automation Market in United States by Equipment ($Million)

- EXHIBIT 178: Canada Warehouse Automation Market Size in US$ Million

- EXHIBIT 179:Warehouse Automation Market in Canada by End-Use Industry ($Million)

- EXHIBIT 180:Warehouse Automation Market in Canada by Equipment ($Million)

- EXHIBIT 181: Western Europe Warehouse Automation Market Size in US$ Million

- EXHIBIT 182: Central & Eastern Europe Warehouse Automation Market Size in US$ Million

- EXHIBIT 183:UK Warehouse Automation Market Size in US$ Million

- EXHIBIT 184:Warehouse Automation Market in United Kingdom by End-Use Industry ($Million)

- EXHIBIT 185:Warehouse Automation Market in United Kingdom by Equipment ($Million)

- EXHIBIT 186: Germany Warehouse Automation Market Size in US$ Million

- EXHIBIT 187:Warehouse Automation Market in Germany by End-Use Industry ($Million)

- EXHIBIT 188:Warehouse Automation Market in Germany by Equipment ($Million)

- EXHIBIT 189: France Warehouse Automation Market Size in US$ Million

- EXHIBIT 190:Warehouse Automation Market in France by End-Use Industry ($Million)

- EXHIBIT 191:Warehouse Automation Market in France by Equipment ($Million)

- EXHIBIT 192: Italy Warehouse Automation Market Size in US$ Million

- EXHIBIT 193:Warehouse Automation Market in Italy by End-Use Industry ($Million)

- EXHIBIT 194:Warehouse Automation Market in Italy by Equipment ($Million)

- EXHIBIT 195: Spain Warehouse Automation Market Size in US$ Million

- EXHIBIT 196:Warehouse Automation Market in Spain, By End-Use Industry ($Million)

- EXHIBIT 197:Warehouse Automation Market in Spain, By Equipment ($Million)

- EXHIBIT 198: Netherlands Warehouse Automation Market Size in US$ Million

- EXHIBIT 199:Warehouse Automation Market in Netherlands, By End-Use Industry ($Million)

- EXHIBIT 200:Warehouse Automation Market in Netherlands, By Equipment ($Million)

- EXHIBIT 201: Nordic Warehouse Automation Market Size in US$ Million

- EXHIBIT 202:Warehouse Automation Market in Nordics, by End-Use Industry ($Million)

- EXHIBIT 203:Warehouse Automation Market in Nordics, by Equipment ($Million)

- EXHIBIT 204: Rest of Western Europe Warehouse Automation Market Size in US$ Million

- EXHIBIT 205:Warehouse Automation Market in Rest of Western Europe by End-Use Industry ($Million)

- EXHIBIT 206:Warehouse Automation Market in Rest of Central and Eastern Europe by End-Use Industry ($Million)

- EXHIBIT 207:Warehouse Automation Market in Rest of Western Europe by Equipment ($Million)

- EXHIBIT 208:Warehouse Automation Market in Rest of Central and Eastern Europe by Equipment ($Million)

- EXHIBIT 209: Asia-Pacific Warehouse Automation Market Size in US$ Million

- EXHIBIT 210: China Warehouse Automation Market Size in US$ Million

- EXHIBIT 211:Warehouse Automation Market in China by End-Use Industry ($Million)

- EXHIBIT 212:Warehouse Automation Market in China by Equipment ($Million)

- EXHIBIT 213: Japan Warehouse Automation Market Size in US$ Million

- EXHIBIT 214:Warehouse Automation Market in Japan by End-Use Industry ($Million)

- EXHIBIT 215:Warehouse Automation Market in Japan by Equipment ($Million)

- EXHIBIT 216: South Korea Warehouse Automation Market Size in US$ Million

- EXHIBIT 217:Warehouse Automation Market in South Korea by End-Use Vertical ($Million)

- EXHIBIT 218:Warehouse Automation Market in South Korea by Equipment ($Million)

- EXHIBIT 219: India Warehouse Automation Market Size in US$ Million

- EXHIBIT 220:Warehouse Automation Market in India by End-Use Industry ($Million)

- EXHIBIT 221:Warehouse Automation Market in India by Equipment ($Million)

- EXHIBIT 222: Australia Warehouse Automation Market Size in US$ Million

- EXHIBIT 223:Warehouse Automation Market in Australia by End-Use Industry ($Million)

- EXHIBIT 224:Warehouse Automation Market in Australia by Equipment ($Million)

- EXHIBIT 225:Southeast Asia Warehouse Automation Market (US$ Million)

- EXHIBIT 226: Middle-East Warehouse Automation Market (US$ Million)

- EXHIBIT 227:Latin America Warehouse Automation Market Size in US$ Million

- EXHIBIT 228: The Top Warehouse Automation Solution Suppliers and their capabilities

- EXHIBIT 229: The Top Supply Chain Software providers and their capabilities

- EXHIBIT 230: AIDC Suppliers and their capabilities

- EXHIBIT 231:Warehouse Automation Market Share (Revenue) – 2025

- EXHIBIT 232: Warehouse Automation Market Share (Revenue) – 2024

- EXHIBIT 233: Warehouse Automation – Top 10 Players Globally

- EXHIBIT 234: Mobile Manipulator – Components and body extension for 2 mobile robots

- List of Tables in Pivot Excel File

- Table 1 Warehouse Automation Market – by Geography (USD Million)

- Table 2 Warehouse Automation Market – by Equipment (USD Million)

- Table 3 Warehouse Automation Market – by End Use Industry (USD Million)

- Table 4 Warehouse Automation Market in United States by Equipment (USD Million)

- Table 5 Warehouse Automation Market in United States by End-Use Industry (USD Million)

- Table 6 Warehouse Automation Market in Canada by Equipment (USD Million)

- Table 7 Warehouse Automation Market in Canada by End-Use Industry (USD Million)

- Table 8 Warehouse Automation Market in Germany by Equipment (USD Million)

- Table 9 Warehouse Automation Market in Germany by End-Use Industry (USD Million)

- Table 10 Warehouse Automation Market in United Kingdom by Equipment (USD Million)

- Table 11 Warehouse Automation Market in United Kingdom by End-Use Industry (USD Million)

- Table 12 Warehouse Automation Market in France by Equipment (USD Million)

- Table 13 Warehouse Automation Market in France by End-Use Industry (USD Million)

- Table 14 Warehouse Automation Market in Italy by Equipment (USD Million)

- Table 15 Warehouse Automation Market in Italy by End-Use Industry (USD Million)

- Table 16 Warehouse Automation Market in Spain by Equipment (USD Million)

- Table 17 Warehouse Automation Market in Spain by End-Use Industry (USD Million)

- Table 18 Warehouse Automation Market in Netherlands by Equipment (USD Million)

- Table 19 Warehouse Automation Market in Netherlands by End-Use Industry (USD Million)

- Table 20 Warehouse Automation Market in Nordics by Equipment (USD Million)

- Table 21 Warehouse Automation Market in Nordics by End-Use Industry (USD Million)

- Table 22 Warehouse Automation Market in Rest of Europe by Equipment (USD Million)

- Table 23 Warehouse Automation Market in Rest of Europe by End-Use Industry (USD Million)

- Table 24 Warehouse Automation Market in Russia by Equipment (USD Million)

- Table 25 Warehouse Automation Market in Russia by End-Use Industry (USD Million)

- Table 26 Warehouse Automation Market in Rest of CEE by Equipment (USD Million)

- Table 27 Warehouse Automation Market in Rest of CEE by End-Use Industry (USD Million)

- Table 28 Warehouse Automation Market in China by Equipment (USD Million)

- Table 29 Warehouse Automation Market in China by End-Use Industry (USD Million)

- Table 30 Warehouse Automation Market in Japan by Equipment (USD Million)

- Table 31 Warehouse Automation Market in Japan by End-Use Industry (USD Million)

- Table 32 Warehouse Automation Market in India by Equipment (USD Million)

- Table 33 Warehouse Automation Market in India by End-Use Industry (USD Million)

- Table 34 Warehouse Automation Market in Australia by Equipment (USD Million)

- Table 35 Warehouse Automation Market in Australia by End-Use Industry (USD Million)

- Table 36 Warehouse Automation Market in Thailand by Equipment (USD Million)

- Table 37 Warehouse Automation Market in Thailand by End-Use Industry (USD Million)

- Table 38 Warehouse Automation Market in Vietnam by Equipment (USD Million)

- Table 39 Warehouse Automation Market in Vietnam by End-Use Industry (USD Million)

- Table 40 Warehouse Automation Market in Singapore by Equipment (USD Million)

- Table 41 Warehouse Automation Market in Singapore by End-Use Industry (USD Million)

- Table 42 Warehouse Automation Market in Indonesia by Equipment (USD Million)

- Table 43 Warehouse Automation Market in Indonesia by End-Use Industry (USD Million)

- Table 44 Warehouse Automation Market in South Korea by Equipment (USD Million)

- Table 45 Warehouse Automation Market in South Korea by End-Use Industry (USD Million)

- Table 46 Warehouse Automation Market in Malaysia by Equipment (USD Million)

- Table 47 Warehouse Automation Market in Malaysia by End-Use Industry (USD Million)

- Table 48 Warehouse Automation Market in Philippines by Equipment (USD Million)

- Table 49 Warehouse Automation Market in Philippines by End-Use Industry (USD Million)

- Table 50 Warehouse Automation Market in Taiwan by Equipment (USD Million)

- Table 51 Warehouse Automation Market in Taiwan by End-Use Industry (USD Million)

- Table 52 Warehouse Automation Market in Rest of Asia Pacific by Equipment (USD Million)

- Table 53 Warehouse Automation Market in Rest of Asia Pacific by End-Use Industry (USD Million)

- Table 54 Warehouse Automation Market in Saudi Arabia by Equipment (USD Million)

- Table 55 Warehouse Automation Market in Saudi Arabia by End-Use Industry (USD Million)

- Table 56 Warehouse Automation Market in UAE by Equipment (USD Million)

- Table 57 Warehouse Automation Market in UAE by End-Use Industry (USD Million)

- Table 58 Warehouse Automation Market in Rest of GCC by Equipment (USD Million)

- Table 59 Warehouse Automation Market in Rest of GCC by End-Use Industry (USD Million)

- Table 60 Warehouse Automation Market in Turkey by Equipment (USD Million)

- Table 61 Warehouse Automation Market in Turkey by End-Use Industry (USD Million)

- Table 62 Warehouse Automation Market in South Africa by Equipment (USD Million)

- Table 63 Warehouse Automation Market in South Africa by End-Use Industry (USD Million)

- Table 64 Warehouse Automation Market in Rest of Middle east & Africa by Equipment (USD Million)

- Table 65 Warehouse Automation Market in Rest of Middle east & Africa by End-Use Industry (USD Million)

- Table 66 Warehouse Automation Market in Argentina by Equipment (USD Million)

- Table 67 Warehouse Automation Market in Argentina by End-Use Industry (USD Million)

- Table 68 Warehouse Automation Market in Brazil by Equipment (USD Million)

- Table 69 Warehouse Automation Market in Brazil by End-Use Industry (USD Million)

- Table 70 Warehouse Automation Market in Mexico by Equipment (USD Million)

- Table 71 Warehouse Automation Market in Mexico by End-Use Industry (USD Million)

- Table 72 Warehouse Automation Market in Rest of South America by Equipment (USD Million)

- Table 73 Warehouse Automation Market in Rest of South America by End-Use Industry (USD Million)

- Table 74 Warehouse Automation Market for Gantry Robots (USD Million)

- Table 75 Warehouse Automation Market for Gantry Robots (USD Million)

- Table 76 Warehouse Automation Market in United States for E-commerce (USD Million)

- Table 77 Warehouse Automation Market in United States for Grocery (USD Million)

- Table 78 Warehouse Automation Market in United States for Apparel (USD Million)

- Table 79 Warehouse Automation Market in United States for General Merchandise (USD Million)

- Table 80 Warehouse Automation Market in United States for Wholesale (USD Million)

- Table 81 Warehouse Automation Market in United States for Food & Beverage (USD Million)

- Table 82 Warehouse Automation Market in United States for Post & Parcel (USD Million)

- Table 83 Warehouse Automation Market in United States for Other (USD Million)

- Table 84 Warehouse Automation Market in Canada for E-commerce (USD Million)

- Table 85 Warehouse Automation Market in Canada for Grocery (USD Million)

- Table 86 Warehouse Automation Market in Canada for Apparel (USD Million)

- Table 87 Warehouse Automation Market in Canada for General Merchandise (USD Million)

- Table 88 Warehouse Automation Market in Canada for Wholesale (USD Million)

- Table 89 Warehouse Automation Market in Canada for Food & Beverage (USD Million)

- Table 90 Warehouse Automation Market in Canada for Post & Parcel (USD Million)

- Table 91 Warehouse Automation Market in Canada for Other (USD Million)

- Table 92 Warehouse Automation Market in United Kingdom for E-commerce (USD Million)

- Table 93 Warehouse Automation Market in United Kingdom for Grocery (USD Million)

- Table 94 Warehouse Automation Market in United Kingdom for Apparel (USD Million)

- Table 95 Warehouse Automation Market in United Kingdom for General Merchandise (USD Million)

- Table 96 Warehouse Automation Market in United Kingdom for Wholesale (USD Million)

- Table 97 Warehouse Automation Market in United Kingdom for Food & Beverage (USD Million)

- Table 98 Warehouse Automation Market in United Kingdom for Post & Parcel (USD Million)

- Table 99 Warehouse Automation Market in United Kingdom for Other (USD Million)

- Table 100 Warehouse Automation Market in Germany for E-commerce (USD Million)

- Table 101 Warehouse Automation Market in Germany for Grocery (USD Million)

- Table 102 Warehouse Automation Market in Germany for Apparel (USD Million)

- Table 103 Warehouse Automation Market in Germany for General Merchandise (USD Million)

- Table 104 Warehouse Automation Market in Germany for Wholesale (USD Million)

- Table 105 Warehouse Automation Market in Germany for Food & Beverage (USD Million)

- Table 106 Warehouse Automation Market in Germany for Post & Parcel (USD Million)

- Table 107 Warehouse Automation Market in Germany for Other (USD Million)

- Table 108 Warehouse Automation Market in France for E-commerce (USD Million)

- Table 109 Warehouse Automation Market in France for Grocery (USD Million)

- Table 110 Warehouse Automation Market in France for Apparel (USD Million)

- Table 111 Warehouse Automation Market in France for General Merchandise (USD Million)

- Table 112 Warehouse Automation Market in France for Wholesale (USD Million)

- Table 113 Warehouse Automation Market in France for Food & Beverage (USD Million)

- Table 114 Warehouse Automation Market in France for Post & Parcel (USD Million)

- Table 115 Warehouse Automation Market in France for Other (USD Million)

- Table 116 Warehouse Automation Market in Italy for E-commerce (USD Million)

- Table 117 Warehouse Automation Market in Italy for Grocery (USD Million)

- Table 118 Warehouse Automation Market in Italy for Apparel (USD Million)

- Table 119 Warehouse Automation Market in Italy for General Merchandise (USD Million)

- Table 120 Warehouse Automation Market in Italy for Wholesale (USD Million)

- Table 121 Warehouse Automation Market in Italy for Food & Beverage (USD Million)

- Table 122 Warehouse Automation Market in Italy for Post & Parcel (USD Million)

- Table 123 Warehouse Automation Market in Italy for Other (USD Million)

- Table 124 Warehouse Automation Market in Spain for E-commerce (USD Million)

- Table 125 Warehouse Automation Market in Spain for Grocery (USD Million)

- Table 126 Warehouse Automation Market in Spain for Apparel (USD Million)

- Table 127 Warehouse Automation Market in Spain for General Merchandise (USD Million)

- Table 128 Warehouse Automation Market in Spain for Wholesale (USD Million)

- Table 129 Warehouse Automation Market in Spain for Food & Beverage (USD Million)

- Table 130 Warehouse Automation Market in Spain for Post & Parcel (USD Million)

- Table 131 Warehouse Automation Market in Spain for Other (USD Million)

- Table 132 Warehouse Automation Market in Netherlands for E-commerce (USD Million)

- Table 133 Warehouse Automation Market in Netherlands for Grocery (USD Million)

- Table 134 Warehouse Automation Market in Netherlands for Apparel (USD Million)

- Table 135 Warehouse Automation Market in Netherlands for General Merchandise (USD Million)

- Table 136 Warehouse Automation Market in Netherlands for Wholesale (USD Million)

- Table 137 Warehouse Automation Market in Netherlands for Food & Beverage (USD Million)

- Table 138 Warehouse Automation Market in Netherlands for Post & Parcel (USD Million)

- Table 139 Warehouse Automation Market in Netherlands for Other (USD Million)

- Table 140 Warehouse Automation Market in Nordics for E-commerce (USD Million)

- Table 141 Warehouse Automation Market in Nordics for Grocery (USD Million)

- Table 142 Warehouse Automation Market in Nordics for Apparel (USD Million)

- Table 143 Warehouse Automation Market in Nordics for General Merchandise (USD Million)

- Table 144 Warehouse Automation Market in Nordics for Wholesale (USD Million)

- Table 145 Warehouse Automation Market in Nordics for Food & Beverage (USD Million)

- Table 146 Warehouse Automation Market in Nordics for Post & Parcel (USD Million)

- Table 147 Warehouse Automation Market in Nordics for Other (USD Million)

- Table 148 Warehouse Automation Market in Russia for E-commerce (USD Million)

- Table 149 Warehouse Automation Market in Russia for Grocery (USD Million)

- Table 150 Warehouse Automation Market in Russia for Apparel (USD Million)

- Table 151 Warehouse Automation Market in Russia for General Merchandise (USD Million)

- Table 152 Warehouse Automation Market in Russia for Wholesale (USD Million)

- Table 153 Warehouse Automation Market in Russia for Food & Beverage (USD Million)

- Table 154 Warehouse Automation Market in Russia for Post & Parcel (USD Million)

- Table 155 Warehouse Automation Market in Russia for Other (USD Million)

- Table 156 Warehouse Automation Market in Rest of Europe for E-commerce (USD Million)

- Table 157 Warehouse Automation Market in Rest of Europe for Grocery (USD Million)

- Table 158 Warehouse Automation Market in Rest of Europe for Apparel (USD Million)

- Table 159 Warehouse Automation Market in Rest of Europe for General Merchandise (USD Million)

- Table 160 Warehouse Automation Market in Rest of Europe for Wholesale (USD Million)

- Table 161 Warehouse Automation Market in Rest of Europe for Food & Beverage (USD Million)

- Table 162 Warehouse Automation Market in Rest of Europe for Post & Parcel (USD Million)

- Table 163 Warehouse Automation Market in Rest of Europe for Other (USD Million)

- Table 164 Warehouse Automation Market in Rest of CEE for E-commerce (USD Million)

- Table 165 Warehouse Automation Market in Rest of CEE for Grocery (USD Million)

- Table 166 Warehouse Automation Market in Rest of CEE for Apparel (USD Million)

- Table 167 Warehouse Automation Market in Rest of CEE for General Merchandise (USD Million)

- Table 168 Warehouse Automation Market in Rest of CEE for Wholesale (USD Million)

- Table 169 Warehouse Automation Market in Rest of CEE for Food & Beverage (USD Million)

- Table 170 Warehouse Automation Market in Rest of CEE for Post & Parcel (USD Million)

- Table 171 Warehouse Automation Market in Rest of CEE for Other (USD Million)

- Table 172 Warehouse Automation Market in China for E-commerce (USD Million)

- Table 173 Warehouse Automation Market in China for Grocery (USD Million)

- Table 174 Warehouse Automation Market in China for Apparel (USD Million)

- Table 175 Warehouse Automation Market in China for General Merchandise (USD Million)

- Table 176 Warehouse Automation Market in China for Wholesale (USD Million)

- Table 177 Warehouse Automation Market in China for Food & Beverage (USD Million)

- Table 178 Warehouse Automation Market in China for Post & Parcel (USD Million)

- Table 179 Warehouse Automation Market in China for Other (USD Million)

- Table 180 Warehouse Automation Market in Japan for E-commerce (USD Million)

- Table 181 Warehouse Automation Market in Japan for Grocery (USD Million)

- Table 182 Warehouse Automation Market in Japan for Apparel (USD Million)

- Table 183 Warehouse Automation Market in Japan for General Merchandise (USD Million)

- Table 184 Warehouse Automation Market in Japan for Wholesale (USD Million)

- Table 185 Warehouse Automation Market in Japan for Food & Beverage (USD Million)

- Table 186 Warehouse Automation Market in Japan for Post & Parcel (USD Million)

- Table 187 Warehouse Automation Market in Japan for Other (USD Million)

- Table 188 Warehouse Automation Market in India for E-commerce (USD Million)

- Table 189 Warehouse Automation Market in India for Grocery (USD Million)

- Table 190 Warehouse Automation Market in India for Apparel (USD Million)

- Table 191 Warehouse Automation Market in India for General Merchandise (USD Million)

- Table 192 Warehouse Automation Market in India for Wholesale (USD Million)

- Table 193 Warehouse Automation Market in India for Food & Beverage (USD Million)

- Table 194 Warehouse Automation Market in India for Post & Parcel (USD Million)

- Table 195 Warehouse Automation Market in India for Other (USD Million)

- Table 196 Warehouse Automation Market in Australia for E-commerce (USD Million)

- Table 197 Warehouse Automation Market in Australia for Grocery (USD Million)

- Table 198 Warehouse Automation Market in Australia for Apparel (USD Million)

- Table 199 Warehouse Automation Market in Australia for General Merchandise (USD Million)

- Table 200 Warehouse Automation Market in Australia for Wholesale (USD Million)

- Table 201 Warehouse Automation Market in Australia for Food & Beverage (USD Million)

- Table 202 Warehouse Automation Market in Australia for Post & Parcel (USD Million)

- Table 203 Warehouse Automation Market in Australia for Other (USD Million)

- Table 204 Warehouse Automation Market in Thailand for E-commerce (USD Million)

- Table 205 Warehouse Automation Market in Thailand for Grocery (USD Million)

- Table 206 Warehouse Automation Market in Thailand for Apparel (USD Million)

- Table 207 Warehouse Automation Market in Thailand for General Merchandise (USD Million)

- Table 208 Warehouse Automation Market in Thailand for Wholesale (USD Million)

- Table 209 Warehouse Automation Market in Thailand for Food & Beverage (USD Million)

- Table 210 Warehouse Automation Market in Thailand for Post & Parcel (USD Million)

- Table 211 Warehouse Automation Market in Thailand for Other (USD Million)

- Table 212 Warehouse Automation Market in Vietnam for E-commerce (USD Million)

- Table 213 Warehouse Automation Market in Vietnam for Grocery (USD Million)

- Table 214 Warehouse Automation Market in Vietnam for Apparel (USD Million)

- Table 215 Warehouse Automation Market in Vietnam for General Merchandise (USD Million)

- Table 216 Warehouse Automation Market in Vietnam for Wholesale (USD Million)

- Table 217 Warehouse Automation Market in Vietnam for Food & Beverage (USD Million)

- Table 218 Warehouse Automation Market in Vietnam for Post & Parcel (USD Million)

- Table 219 Warehouse Automation Market in Vietnam for Other (USD Million)

- Table 220 Warehouse Automation Market in Singapore for E-commerce (USD Million)

- Table 221 Warehouse Automation Market in Singapore for Grocery (USD Million)

- Table 222 Warehouse Automation Market in Singapore for Apparel (USD Million)

- Table 223 Warehouse Automation Market in Singapore for General Merchandise (USD Million)

- Table 224 Warehouse Automation Market in Singapore for Wholesale (USD Million)

- Table 225 Warehouse Automation Market in Singapore for Food & Beverage (USD Million)

- Table 226 Warehouse Automation Market in Singapore for Post & Parcel (USD Million)

- Table 227 Warehouse Automation Market in Singapore for Other (USD Million)

- Table 228 Warehouse Automation Market in Indonesia for E-commerce (USD Million)

- Table 229 Warehouse Automation Market in Indonesia for Grocery (USD Million)

- Table 230 Warehouse Automation Market in Indonesia for Apparel (USD Million)

- Table 231 Warehouse Automation Market in Indonesia for General Merchandise (USD Million)

- Table 232 Warehouse Automation Market in Indonesia for Wholesale (USD Million)

- Table 233 Warehouse Automation Market in Indonesia for Food & Beverage (USD Million)

- Table 234 Warehouse Automation Market in Indonesia for Post & Parcel (USD Million)

- Table 235 Warehouse Automation Market in Indonesia for Other (USD Million)

- Table 236 Warehouse Automation Market in South Korea for E-commerce (USD Million)

- Table 237 Warehouse Automation Market in South Korea for Grocery (USD Million)

- Table 238 Warehouse Automation Market in South Korea for Apparel (USD Million)

- Table 239 Warehouse Automation Market in South Korea for General Merchandise (USD Million)

- Table 240 Warehouse Automation Market in South Korea for Wholesale (USD Million)

- Table 241 Warehouse Automation Market in South Korea for Food & Beverage (USD Million)

- Table 242 Warehouse Automation Market in South Korea for Post & Parcel (USD Million)

- Table 243 Warehouse Automation Market in South Korea for Other (USD Million)

- Table 244 Warehouse Automation Market in Malaysia for E-commerce (USD Million)

- Table 245 Warehouse Automation Market in Malaysia for Grocery (USD Million)

- Table 246 Warehouse Automation Market in Malaysia for Apparel (USD Million)

- Table 247 Warehouse Automation Market in Malaysia for General Merchandise (USD Million)

- Table 248 Warehouse Automation Market in Malaysia for Wholesale (USD Million)

- Table 249 Warehouse Automation Market in Malaysia for Food & Beverage (USD Million)

- Table 250 Warehouse Automation Market in Malaysia for Post & Parcel (USD Million)

- Table 251 Warehouse Automation Market in Malaysia for Other (USD Million)

- Table 252 Warehouse Automation Market in Philippines for E-commerce (USD Million)

- Table 253 Warehouse Automation Market in Philippines for Grocery (USD Million)

- Table 254 Warehouse Automation Market in Philippines for Apparel (USD Million)

- Table 255 Warehouse Automation Market in Philippines for General Merchandise (USD Million)

- Table 256 Warehouse Automation Market in Philippines for Wholesale (USD Million)

- Table 257 Warehouse Automation Market in Philippines for Food & Beverage (USD Million)

- Table 258 Warehouse Automation Market in Philippines for Post & Parcel (USD Million)

- Table 259 Warehouse Automation Market in Philippines for Other (USD Million)

- Table 260 Warehouse Automation Market in Taiwan for E-commerce (USD Million)

- Table 261 Warehouse Automation Market in Taiwan for Grocery (USD Million)

- Table 262 Warehouse Automation Market in Taiwan for Apparel (USD Million)

- Table 263 Warehouse Automation Market in Taiwan for General Merchandise (USD Million)

- Table 264 Warehouse Automation Market in Taiwan for Wholesale (USD Million)

- Table 265 Warehouse Automation Market in Taiwan for Food & Beverage (USD Million)

- Table 266 Warehouse Automation Market in Taiwan for Post & Parcel (USD Million)

- Table 267 Warehouse Automation Market in Taiwan for Other (USD Million)

- Table 268 Warehouse Automation Market in Rest of Asia Pacific for E-commerce (USD Million)

- Table 269 Warehouse Automation Market in Rest of Asia Pacific for Grocery (USD Million)

- Table 270 Warehouse Automation Market in Rest of Asia Pacific for Apparel (USD Million)

- Table 271 Warehouse Automation Market in Rest of Asia Pacific for General Merchandise (USD Million)

- Table 272 Warehouse Automation Market in Rest of Asia Pacific for Wholesale (USD Million)

- Table 273 Warehouse Automation Market in Rest of Asia Pacific for Food & Beverage (USD Million)

- Table 274 Warehouse Automation Market in Rest of Asia Pacific for Post & Parcel (USD Million)

- Table 275 Warehouse Automation Market in Rest of Asia Pacific for Other (USD Million)

- Table 276 Warehouse Automation Market in Saudi Arabia for E-commerce (USD Million)

- Table 277 Warehouse Automation Market in Saudi Arabia for Grocery (USD Million)

- Table 278 Warehouse Automation Market in Saudi Arabia for Apparel (USD Million)

- Table 279 Warehouse Automation Market in Saudi Arabia for General Merchandise (USD Million)

- Table 280 Warehouse Automation Market in Saudi Arabia for Wholesale (USD Million)

- Table 281 Warehouse Automation Market in Saudi Arabia for Food & Beverage (USD Million)